Studs-In vs. Studs-Out: Demystifying Condo Association Coverage

Adams Kotel

Published on

Owning a condominium is a masterclass in shared responsibility. You enjoy the privacy of your own sanctuary, while sharing the financial burden of the roof, the elevators, and the landscaping with your neighbors through the Homeowners Association (HOA). In theory, this arrangement is the pinnacle of modern, efficient living. In practice, however, the moment a disaster strikes—be it a kitchen fire, a burst pipe, or a severe windstorm—this shared responsibility devolves into a highly contentious, incredibly stressful jurisdictional battle.

The core of the conflict always boils down to a single question: Where exactly does the HOA's insurance end, and where does your personal insurance begin?

In the insurance industry, this boundary line is often described using colloquial shorthand that baffles the average consumer. Search data from Bing in 2026 reveals a surge of confused condo owners desperately typing queries like, "explain studs in vs. studs out in condos" and "what is walls in ho6 insurance?"

If you do not know the answer to these questions regarding your specific unit, your financial future is in severe jeopardy. If you assume the HOA covers your interior, but their policy stops at the raw framing, you could be left personally responsible for $100,000 or more in reconstruction costs after a fire.

This exhaustive, 2,200-word masterclass will serve as your ultimate translator for condo insurance jargon. Building upon the mathematical framework we established in The Ultimate HO-6 Coverage Calculator, we will dissect the legal definitions of "Studs-In" and "Studs-Out," explain the devastating "Betterments and Improvements" gap, and provide a strategic protocol for auditing your HOA's governing documents to build an impenetrable financial shield.

Part 1: The Architectural Boundary—What Do You Actually Own?

To understand condo insurance, you must first forget how single-family homeownership works. When you buy a house, you own the land, the foundation, the exterior siding, and the roof. When you buy a condo, you do not own the building. Legally speaking, you own a three-dimensional box of "airspace."

The perimeter of that airspace is defined by your HOA's Covenants, Conditions, and Restrictions (CC&Rs). The insurance coverage must perfectly mirror those legal boundaries. If there is a gap between what the HOA's Master Policy covers and what your personal HO-6 policy covers, that gap becomes a "Dead Zone" where neither insurance company will pay. You will be forced to pay out of pocket.

The industry categorizes Master Policies into three broad types, which correspond directly to the "Studs" terminology.

Part 2: "Studs-Out" (The "Bare Walls" Policy)

When a real estate agent or an insurance broker refers to a "Studs-Out" or "Bare Walls-In" Master Policy, they are describing the most restrictive, least generous type of HOA coverage. It places a massive financial burden squarely on the shoulders of the individual unit owner.

The Boundary Line

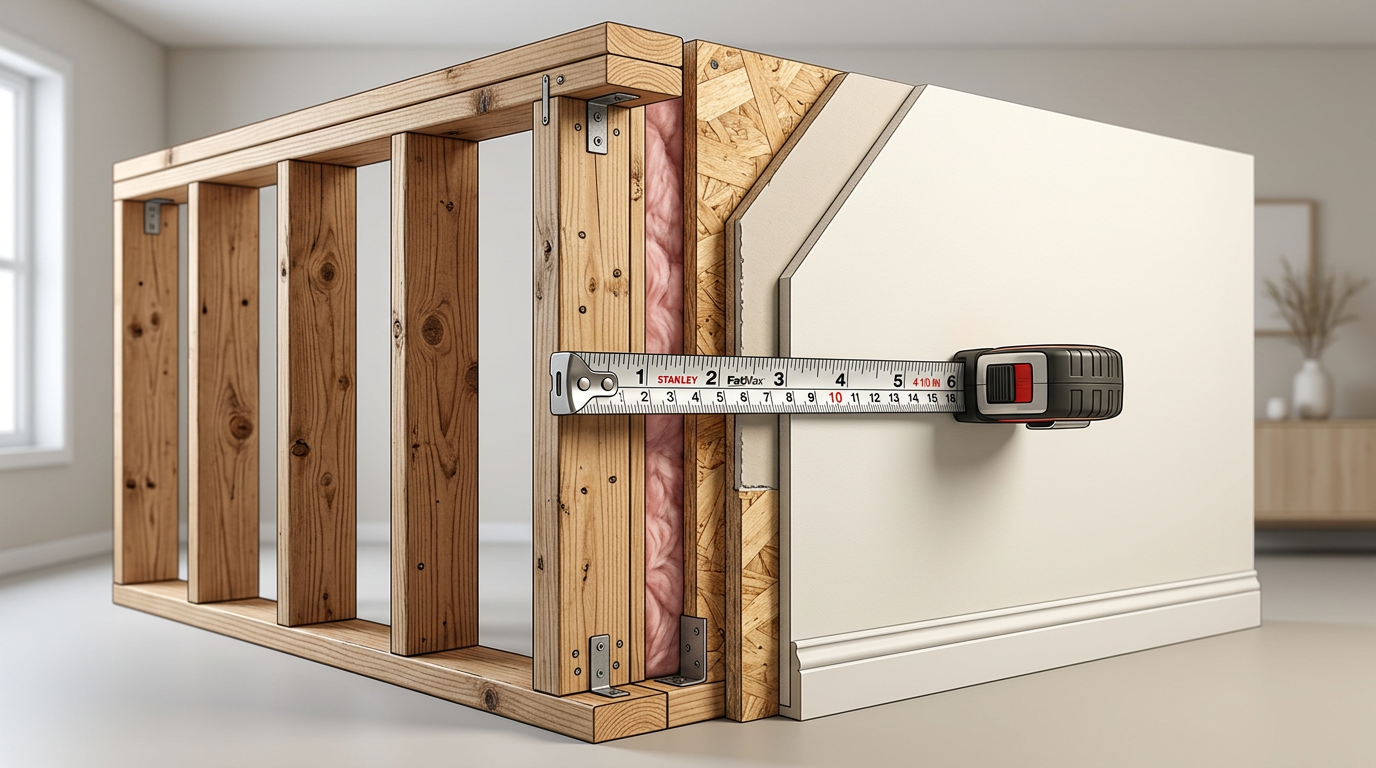

Imagine standing in your living room and stripping away the paint, the drywall, the insulation, and the flooring until you are staring at the raw, bare wooden framing (the studs) and the concrete subfloor.

- The Master Policy (Studs-Out): The HOA's insurance covers everything from the studs outward. It covers the wooden framing, the exterior brick or siding, the roof, and the utility pipes and wires running inside the wall cavity between units.

- Your HO-6 Policy (Studs-In): You are responsible for everything from the studs inward.

The Financial Danger

If a fire guts your unit, the HOA's Master Policy will rebuild the raw, empty wooden box. It will look like a construction site. You, via your personal HO-6 Dwelling Coverage (Coverage A), must pay to install the insulation, hang and tape the drywall, paint the walls, lay the carpet or hardwood, and install the plumbing fixtures, lighting, and kitchen cabinets.

If you live in a "Bare Walls" or "Studs-Out" complex, a standard $10,000 Coverage A limit on your personal policy is a mathematical catastrophe. You likely need $100,000 to $200,000 in Coverage A to rebuild a modern condo interior from the studs in 2026.

Part 3: "Studs-In" (The "Single Entity" Policy)

When professionals refer to a "Studs-In" policy, they are usually referring to a "Single Entity" Master Policy. This is the most common middle-ground structure in the American condo market.

The Boundary Line

This policy extends the HOA's insurance umbrella past the raw framing and into the living space.

- The Master Policy: It covers the exterior, the framing, the drywall, the paint, and all the interior fixtures (cabinets, flooring, plumbing) exactly as they were originally built by the developer.

- Your HO-6 Policy: You are responsible only for your personal belongings and any upgrades made to the unit since it was built.

The "Improvements and Betterments" Trap

This is the hidden trap of the Studs-In/Single Entity policy. It covers the original specifications. Let's say your condo was built in 2005 with cheap builder-grade carpet and laminate countertops. Last year, you (or a previous owner) spent $40,000 upgrading the unit with Brazilian hardwood floors and custom quartz countertops.

If a pipe bursts and ruins the kitchen and floors:

- The HOA Master Policy will only pay the amount required to install the 2005-era cheap carpet and laminate.

- If you want your hardwood and quartz back, your HO-6 policy must have an "Improvements and Betterments" limit high enough to cover the price difference between the cheap original materials and your luxury upgrades.

Part 4: The "All-In" Policy (The Rare Unicorn)

The third, and most generous, variation is the "All-In" or "All-Inclusive" Master Policy.

- The Boundary Line: The HOA Master Policy covers the entire building, the drywall, and the interior fixtures, including any upgrades made by the unit owners.

- Your Responsibility: If your HOA has an "All-In" policy, your HO-6 only needs to cover your personal property (Coverage C) and your personal liability (Coverage E). Your Dwelling Coverage (Coverage A) can be kept very low (e.g., $10,000) just to act as a buffer.

Warning: While "All-In" policies exist, they are becoming increasingly rare in 2026 as HOAs struggle with surging commercial insurance premiums. Many HOAs are aggressively amending their bylaws to shift from "All-In" to "Bare Walls" to save money on the Master Policy, silently transferring the risk to the unit owners.

Part 5: The Primary vs. Excess Conflict

Understanding the "Studs" boundary is only the first step. You must also understand the sequence of payment when a claim occurs. This is governed by the "Primary/Excess" clause in the HOA bylaws.

If a fire damages your drywall, and your complex has a "Single Entity" (Studs-In) policy, both the Master Policy and your HO-6 policy technically provide coverage. Who pays first?

- Master Policy is Primary: In most modern HOAs, the bylaws state that the Master Policy is "Primary." The HOA's insurance pays first, up to its limits, and your HO-6 policy acts as "Excess," stepping in only if the HOA policy runs out of money or doesn't cover upgrades.

- Unit Owner is Primary: In some older or highly restrictive HOAs, the bylaws force the Unit Owner's policy to be "Primary" for anything inside the unit. If this is the case, your HO-6 policy takes the initial hit, which can lead to severe rate hikes on your personal insurance, even if the fire started outside your unit.

Part 6: The Ultimate Threat—The Master Policy Deductible

There is a final variable that routinely destroys condo owners financially, regardless of whether the policy is Studs-In or Studs-Out. It is the Master Policy Deductible.

To keep their commercial premiums affordable, HOA boards in 2026 are selecting astronomically high deductibles on the Master Policy—often $25,000, $50,000, or even $100,000 per occurrence.

The "Chargeback" Nightmare

Imagine a severe windstorm damages the roof (a common peril discussed in our roof leak guide). The roof is strictly the HOA's responsibility. The repair costs $150,000. The HOA Master Policy has a $50,000 deductible. The insurance company pays $100,000.

Where does the HOA get the remaining $50,000 to fix the roof? They issue a Special Assessment to the unit owners. If there are 10 units in the building, you will receive a bill in the mail demanding $5,000 immediately.

Even worse, if a fire starts in your unit (e.g., a grease fire), many bylaws allow the HOA to charge the entire $50,000 Master Deductible directly back to you, arguing that you were the negligent cause of the claim.

The Shield: Loss Assessment Coverage

To protect yourself from this, you must explicitly demand Loss Assessment Coverage on your HO-6 policy. As we emphasize in all our condo advice, the standard $1,000 limit included in basic policies is useless. You must increase this limit to at least $25,000 or $50,000. It is incredibly cheap (often $20-$30 a year) and is the only defense against a bankrupting HOA chargeback.

Part 7: The "Insurance Audit" Protocol for Condo Owners

You cannot guess your coverage. You must perform a forensic insurance audit. Follow these three steps today:

Step 1: Obtain the Documents Email your HOA property manager and request two documents:

- The Certificate of Insurance (COI) for the Master Policy.

- The CC&Rs (Declarations) section pertaining to "Insurance" and "Maintenance Responsibilities."

Step 2: Read the Definitions Search the CC&Rs for the definition of the "Unit." Does it say the unit boundary is the "unfinished interior surfaces of the perimeter walls" (Bare Walls)? Or does it include "wallboard, plaster, and paint" (Single Entity)?

Step 3: Consult the Broker Do not try to interpret 50 pages of legalese alone. Take these documents to your independent insurance broker. A professional broker will read the CC&Rs, identify the "Studs" boundary, identify the Primary/Excess rules, note the Master Deductible, and custom-build your HO-6 policy to interlock perfectly with the HOA's coverage.

Part 8: Renting Your Condo? The Rules Change Entirely

If you decide to move out and rent your condo to a tenant, everything we just discussed is nullified. Your HO-6 is for an owner-occupied unit. The moment a tenant moves in, you must convert your policy. We detail this critical transition in our guide, The Condo Investor's Guide to Landlord Policies. Failing to update your occupancy status is the easiest way for an insurer to deny a massive interior damage claim.

Conclusion: Trusting the Contract, Not the Board

Condominium living relies on a delicate balance of trust—trust that your neighbors won't start a fire, trust that the HOA board will maintain the roof, and trust that the insurance policies will respond when needed. In the high-stakes environment of 2026, trust is a poor substitute for a watertight legal contract.

The difference between "Studs-In" and "Studs-Out" is not just architectural trivia; it is the difference between a minor inconvenience and a financial disaster. It dictates whether you owe a contractor $2,000 or $120,000.

By aggressively auditing your HOA's Master Policy, accurately calculating your "Betterments and Improvements," and fortifying your HO-6 policy with high Loss Assessment limits, you eliminate the "Dead Zones" in your coverage. At Surety Insights, we believe that Clarity is Coverage. Do not assume you are protected. Verify the boundaries, engineer the perfect HO-6 shield, and enjoy your condo with the absolute certainty that your equity is secure.

Share this article

About the Author

Adams Kotel

Lead Insurance Analyst

Adams has over 15 years of experience in the insurance industry, specializing in personal line products. He is passionate about demystifying complex insurance topics and helping consumers make educated decisions.

Related Articles

Water Backup vs. Flood Insurance: Decoding Basement Water Claims

Water is ruining your basement floor, but where did it come from? We explain the critical legal difference between "Flood," "Water Backup," and "Seepage," and why your claim might be denied.

Adams Kotel

Pet Damage vs. Pet Liability: What Your Home Insurance Actually Covers

If your dog chews a hole in your sofa, you pay for it. If your dog chews a hole in your neighbor's sofa, insurance pays. We explain the strict boundary between pet damage and pet liability.

Josef Bako