Long-Term Roof Leaks: Will Your Home Insurance Cover the Damage?

Adams Kotel

Published on

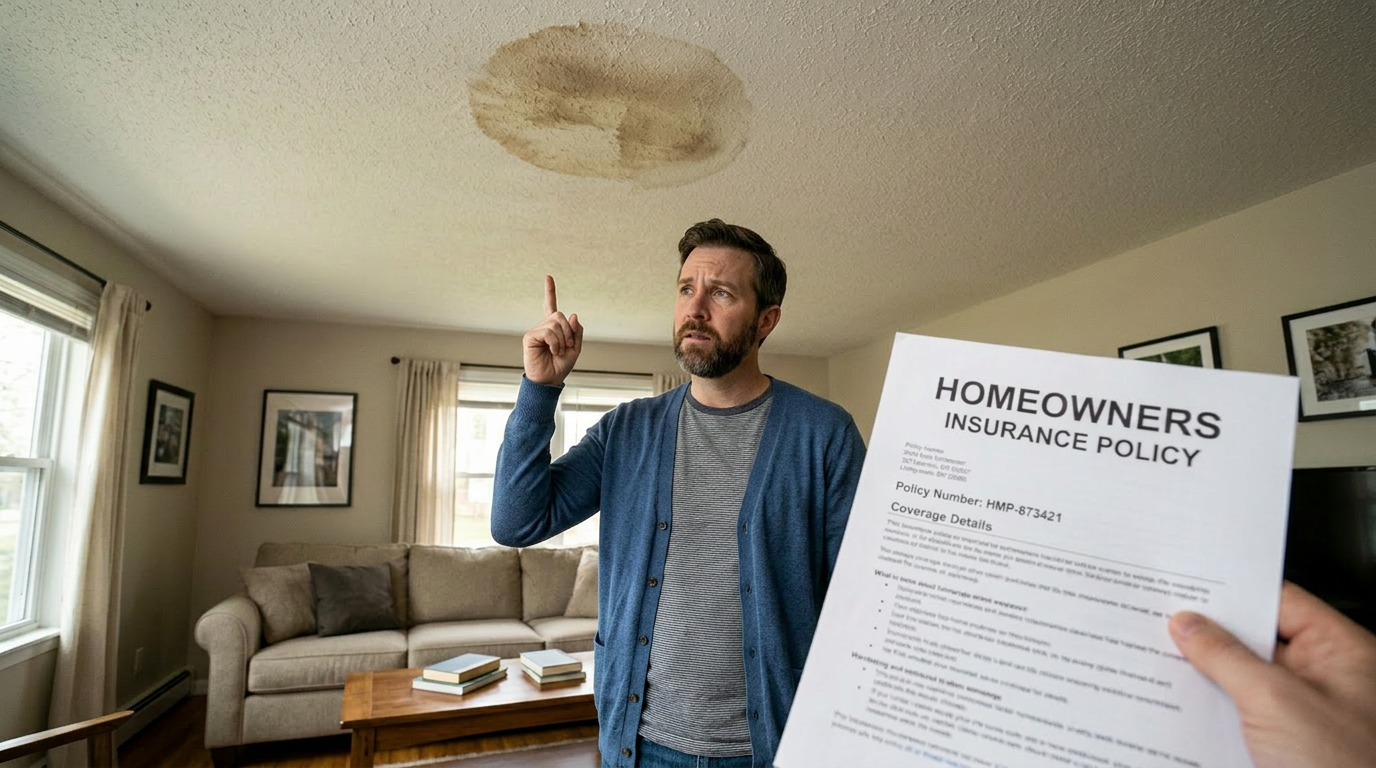

There are few moments in homeownership as universally dreaded as looking up at your ceiling and spotting the telltale sign of water intrusion: a creeping, discolored, brownish-yellow ring. Your stomach drops. But the panic truly sets in when you touch the drywall and realize it is soft, crumbling, and covered in mildew. This isn't a fresh leak from last night's thunderstorm; this is a long-term roof leak that has been silently dripping into your attic and soaking your insulation for weeks, months, or perhaps even years.

You immediately reach for your phone to call a roofer and your insurance agent. However, a creeping doubt enters your mind. You've heard the horror stories. You've read the fine print about "routine maintenance." You begin searching the internet, frantically typing queries like, "learn more about the essentials of long-term roof leak insurance coverage" or "will insurance pay if a roof leak is old?"

The search data from Bing in the spring of 2026 shows that this is one of the most highly searched, yet poorly understood, crises in the property insurance landscape. The anxiety is justified. In the modern, hyper-strict insurance market, reporting a long-term, gradual water leak is akin to walking through a legal minefield. Insurance adjusters are trained to look for specific "trigger words" that allow them to categorize the damage as a "maintenance failure," which results in an immediate, absolute denial of your claim.

However, a long-term leak is not an automatic death sentence for your claim. The success of your financial recovery depends entirely on understanding the technical language of your policy, the legal doctrine of "Proximate Cause," and the critical concept of "Consequential Damage." This exhaustive 2,200-word masterclass will provide you with the professional roadmap you need. We will decode the dreaded 14-Day Rule, explain how to differentiate the roof repair from the interior repair, and teach you how to advocate for a fair settlement when the water damage has been hiding in plain sight.

Part 1: The Actuarial Wall—"Sudden and Accidental" vs. "Wear and Tear"

To understand how an insurance company views a roof leak, you must first understand the fundamental premise of a homeowners insurance contract (the HO-3 policy). As we discussed in our guide to standard policy coverages, insurance is a transfer of risk for unforeseeable catastrophes. It is not a home warranty, and it is not a maintenance plan.

Every property claim evaluation begins with two opposing concepts:

1. The "Sudden and Accidental" Standard

Insurance covers events that happen instantaneously and without warning. If a severe windstorm rips a swath of shingles off your roof on a Tuesday, and rain pours into your living room on that same Tuesday, the cause of the leak is undeniably "sudden and accidental." The insurance company will pay to replace the missing shingles, the wet drywall, and the ruined hardwood floors (subject to your deductible).

2. The "Wear and Tear" Exclusion

Conversely, every standard policy contains an absolute exclusion for "wear and tear, marring, deterioration, latent defect, or inherent vice." Asphalt shingles age. Sun bakes them, thermal expansion cracks them, and the adhesive eventually fails. If your roof is 20 years old and a bald spot simply wears through, allowing rain to slowly seep into the attic over a period of six months, the insurance company views this as a failure of homeowner maintenance.

The Rule of Thumb: If the roof leaked because it simply "got old," the insurance company will never pay to replace the roof itself.

Part 2: The Saving Grace—"Consequential Damage"

If you discover a long-term leak caused by an aging roof, you might assume your entire claim is void. This is a common and expensive misunderstanding. You must separate the claim into two distinct parts: the Source (the roof) and the Result (the interior).

This introduces one of the most vital legal concepts in insurance: Consequential Damage (sometimes called Resulting Damage).

Most modern policies contain an "Ensuing Loss" clause. It dictates that while the cause of the leak (the worn-out shingles) is excluded from coverage, the ensuing water damage to the interior of the home is covered.

- The Scenario: A flashing seal around your chimney rusts away over five years. It has been slowly dripping water behind the walls of your upstairs bedroom. You didn't know it was happening until the paint began to peel yesterday.

- The Adjuster's Verdict: The adjuster will deny the claim to fix the chimney flashing, citing "wear and tear and deterioration." The cost of the roofer ($500) is on you. However, the adjuster will approve the claim for the $15,000 required to tear out the wet drywall, replace the rotted studs, and repaint the bedroom.

The Strategic Takeaway: Do not abandon a massive interior water damage claim just because your roofer told you the leak was caused by an "old roof." The interior damage is often still a covered peril.

Part 3: The Dreaded "14-Day Rule" (The Gradual Damage Trap)

While the Ensuing Loss clause provides a safety net, the insurance industry has built a trap door right beneath it. It is known as the Continuous or Repeated Seepage or Leakage Exclusion—commonly referred to in the industry as the "14-Day Rule."

If you perform an insurance audit and read the fine print of your policy, you will likely find language stating that the policy does not cover water damage that occurs over a period of "14 days or more" (some strict policies now say 13 days).

How Adjusters Weaponize the 14-Day Rule

If you call the claims hotline and say, "I've had this water stain on my ceiling for a couple of months, but it just started getting worse today," you have just handed the adjuster a verbal confession. They will immediately deny the entire claim—including the interior damage—citing the 14-day continuous seepage exclusion.

But what if the leak was hidden? What if the water was dripping into a sealed attic cavity or behind a fiberglass shower surround, and you had absolutely no visual evidence until the water finally breached the drywall on day 45?

The "Hidden Damage" Defense

In 2026, the battle over "hidden" long-term leaks is one of the most fiercely litigated areas of property insurance.

- The Insurer's Argument: The policy language is absolute. If the water leaked for more than 14 days, it is excluded, regardless of whether you could see it or not.

- The Homeowner's Defense: You must argue that the damage you are claiming is only the damage that occurred after it became visible. More importantly, in many states, courts have ruled that the 14-day exclusion implies a "duty to act." If the leak was genuinely hidden behind walls and you acted immediately upon discovering it, a skilled Public Adjuster or attorney can often force the insurer to cover the damage.

The Golden Rule of Claim Reporting: When reporting a leak, deal strictly in facts regarding what you know. Do not guess how long it has been leaking. The accurate statement is: "I discovered a water stain on my ceiling this morning, and I am reporting it immediately." Let the experts determine the timeline.

Part 4: Proximate Cause—When Wind Hides the Evidence

There is a scenario where the insurance company will pay for both the interior damage AND the roof replacement, even if the leak has been going on for a long time. It all comes down to establishing the Proximate Cause.

Imagine you discover a massive, long-term leak in your attic in April. The adjuster inspects the roof and sees that the shingles are 15 years old. They prepare to deny the roof replacement based on "wear and tear."

However, you hire an independent roofing contractor to inspect the property. The contractor lifts the shingles and finds "creased" and "lifted" tabs that exactly match the forensic signature of a severe windstorm that hit your zip code back in November.

- The Legal Argument: The proximate cause (the initial event that set the chain of damage into motion) was the covered windstorm in November. The wind broke the seal of the shingles, which allowed the snow and rain over the next five months to slowly rot the decking and leak into the attic.

- The Result: Because the origin of the failure was a sudden and accidental covered peril (wind), the insurance company is legally obligated to replace the wind-damaged roof slope, the rotted decking, and all the interior long-term water damage.

This highlights why you should never accept a field adjuster's initial "wear and tear" denial without getting a second opinion from a licensed roofing professional who understands storm forensics.

Part 5: The Mold Complication (The Bio-Hazard Sub-Limit)

If water has been leaking into a dark, warm, insulated space for several months, there is a 99% probability that you have a secondary problem: Mold.

As we explored in our definitive guide, The Mold Trap, insurance companies aggressively limit their exposure to fungal growth. If the adjuster determines that the long-term roof leak is covered (either via ensuing loss or wind damage), they must also address the mold.

- The Cap: Your standard HO-3 policy likely has a strict "Fungi, Wet or Dry Rot, or Bacteria" sub-limit. In 2026, this is typically capped at $10,000.

- The Danger: If a roof has been leaking for a year into an attic, the cost to remediate the mold (using negative pressure containment, HEPA scrubbing, and hazmat removal) can easily exceed $30,000. The insurer will pay the first $10,000, and you will be personally responsible for the remaining $20,000 shortfall.

- The Mitigation: This is why it is absolutely vital to verify your policy limits today. If you only have $10,000 in mold coverage, call your independent broker immediately and ask to "buy up" the mold endorsement to $50,000. It is a cheap endorsement that saves homeowners from bankruptcy during long-term leak claims.

Part 6: The "ACV Roof Schedule" Penalty

Even if you successfully prove that a windstorm caused the long-term leak and the insurer agrees to replace the roof, you must be aware of the valuation trap that has taken over the 2026 market.

As we detailed in The Hidden Clause Costing Homeowners Thousands, many policies now include an ACV Roof Schedule. If your roof is 15 years old, the policy will not pay the full $20,000 to replace it. Instead, they will consult a depreciation schedule and may only pay you 40% of the replacement cost (e.g., $8,000). You will be forced to pay the $12,000 difference out of pocket to get the new roof installed so the interior stops leaking.

When fighting a long-term leak claim, you must review your declarations page to see if you have "Replacement Cost Value" (RCV) or "Actual Cash Value" (ACV) on the roof surface.

Part 7: Step-by-Step Protocol for Filing a Long-Term Leak Claim

If you discover a severe, long-term water stain today, do not panic, but do not delay. Follow this exact protocol to protect your financial interests:

- Stop the Bleeding: You have a legal "duty to mitigate." If water is actively dripping, place buckets, move furniture, and lay down tarps. If you need to pay a roofer $300 to put a temporary emergency tarp on the roof to stop the leak, do it immediately. Save the receipt; the insurer will reimburse you.

- Document the Discovery: Take wide-angle and close-up photos of the water stain, the damaged furniture, and the exterior of the roof (from the ground). Note the exact date and time you discovered the damage.

- Hire a Professional Diagnostician: Before calling the insurance company, consider paying a highly rated local roofer to inspect the roof. Ask them: "Is this leak due to age, or is there evidence of wind, hail, or a falling tree limb?" Knowing the proximate cause before you speak to the adjuster gives you immense leverage.

- File the Claim Carefully: When you call the FNOL (First Notice of Loss) department, stick to the facts. "I discovered a water leak causing damage to my living room ceiling today. I have tarped the roof to prevent further damage and need an adjuster to inspect." Do not speculate on how long it has been leaking.

- Do Not Discard Evidence: If you have to tear down a piece of wet drywall to stop a mold bloom, do not throw it in the trash. The adjuster must see the physical evidence to authorize the payout.

Conclusion: Ignorance is Not an Exclusion

A long-term roof leak is a stressful, complex, and highly technical insurance event. The industry has constructed a labyrinth of exclusions—wear and tear, the 14-day rule, mold sub-limits, and ACV schedules—designed to shield their profit margins from the slow decay of residential real estate.

However, your homeowners policy remains a powerful financial shield if you know how to wield it. By understanding the critical distinction between the cause of the leak and the consequential interior damage, and by aggressively investigating the true proximate cause with independent professionals, you can successfully navigate the actuarial wall.

At Surety Insights, we believe that Clarity is Coverage. Do not accept a blanket denial from a desk adjuster who claims your leak is "too old" to be covered. Demand an investigation into ensuing loss. Protect your equity, document your discoveries immediately, and force the insurance contract to honor the protection you have paid for. Your roof may have failed, but with the right strategy, your financial foundation will remain perfectly intact.

Share this article

About the Author

Adams Kotel

Lead Insurance Analyst

Adams has over 15 years of experience in the insurance industry, specializing in personal line products. He is passionate about demystifying complex insurance topics and helping consumers make educated decisions.

Related Articles

Water Backup vs. Flood Insurance: Decoding Basement Water Claims

Water is ruining your basement floor, but where did it come from? We explain the critical legal difference between "Flood," "Water Backup," and "Seepage," and why your claim might be denied.

Adams Kotel

Pet Damage vs. Pet Liability: What Your Home Insurance Actually Covers

If your dog chews a hole in your sofa, you pay for it. If your dog chews a hole in your neighbor's sofa, insurance pays. We explain the strict boundary between pet damage and pet liability.

Josef Bako